Nvidia will surge another 22%, and is still cheap compared to peers despite nearly doubling this year, Goldman Sachs says

-

Nvidia stock still has 22% upside, even after its near-doubling this year, according to Goldman Sachs.

-

The bank argued that Nvidia’s valuation is still relatively cheap given its fast growth rate.

-

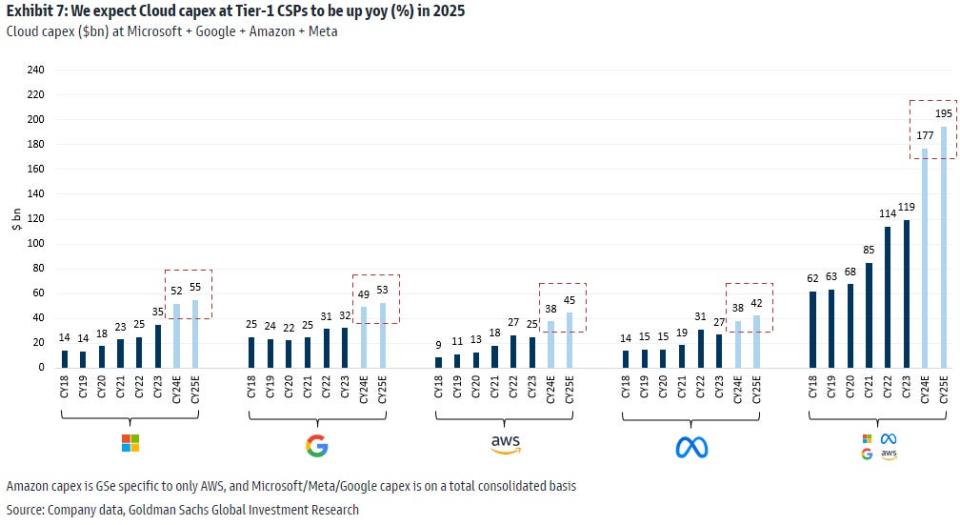

Goldman was encouraged by strong spending trends on AI infrastructure by mega-cap tech giants.

Nvidia stock still has plenty of upside even after its year-to-date rally of 81%, according to a Tuesday note from Goldman Sachs.

The bank raised its Nvidia price target to $1,100 from $1,000, representing potential upside of 22% from current levels.

According to Goldman, Nvidia stock still trades at a relatively attractive valuation compared to its peers given how quickly it is growing and how durable those growth trends look in the coming years.

“We see positive EPS revisions driving another leg up in the stock, especially with NVDA trading at 35x or only a 36% premium to our coverage universe vs. its past 3-year median premium of 160%,” Goldman Sachs analyst Toshiya Hari said.

Hari was specifically encouraged by recent comments from the mega-cap tech giants, which suggested on their earnings call that they will be spending even more money on AI infrastructure in 2025, following an elevated year of investment in 2024.

Those investments should power continued revenue and profit growth at Nvidia, especially with its next-generation Blackwell AI chip set to be released later this year. Nvidia will report its earnings results on May 22 after the market close.

“Notable intra-quarter data points that support the view that AI spending is likely to continue beyond 2024 include” commentary from tech-focused companies, Hari said.

1. TSMC reiterated its near- and long-term outlooks for the AI market, and expects server AI processor revenue to more than double year-over-year.

2. Tier-1 hyperscalers like Amazon and Meta Platforms said or implied that AI-related capital investments are likely to increase in 2025 from an already elevated base in 2024.

3. Some AI hyperscalers and enterprise software companies highlighted early signs of AI monetization.

4. AMD raised its 2024 revenue guidance for its AI-focused GPU chip, the Mi300 to $4 billion from $3.5 billion.

5. Super Micro Computer reported strong revenue growth and a record backlog driven by elevated demand for AI servers.

And while competition is starting to encroach on Nvidia’s GPU business via AMD’s new chip and in-house chip design from mega-cap tech companies, that won’t be enough to knock down the company, according to Hari.

“We believe Nvidia will remain the de facto industry standard for the foreseeable future given its competitive advantage that spans its hardware and software capabilities as well as the installed base and eco-system it has built over multiple decades, and the pace at which it is and will be innovating over the next several years,” Hari said.

Read the original article on Business Insider

Source link